Telephone No. 325-1184

Email address: This email address is being protected from spambots. You need JavaScript enabled to view it.

Republic Act No. 7160, known as the Local Government Code of 1991, specifically Section 3(b) provides that there shall be established in every local government unit an accountable, efficient, and dynamic organizational structure and operating mechanism that will meet the priority needs and service requirements of its communities.

Paragraph 2 of CSC Memorandum Circular No. 19 S. 1992 otherwise known as “Guidelines and standards in the establishment of organizational structures and staffing patterns in Local Government Units provides that It is therefore the responsibility of every local government unit to design, approve and implement the organizational structure and staffing pattern in accordance with the guidelines and standards.

Section 2 of Republic Act No. 3456, the internal Auditing Act of 1962 as amended by RA 4177, There shall be created, organized, and operated in all branches, subdivisions and instrumentalities of the government, Internal Audit Services which shall assist management to achieve an efficient and effective fiscal administration and performance of agency affairs and functions;

Office of the President (OP) Administrative Order (AO) No. 119 dated 29 March 1989 as amended by OP AO No. 278 dated 28 April 1992 (Directing the Strengthening of the Internal Control Systems of Government Offices, Agencies, Government owned and Controlled Corporations, Including Government Financial Institutions, State Universities and Colleges and Local Government Units), mandated government offices and agencies to strengthen their Internal Control System and directed to organize Internal Audit Service (IAS) in their respective offices;

Administrative Order No. 70 dated 14 April 2003 (Strengthening of the Internal Control Systems of Government Offices, Agencies, Government owned and Controlled Corporations, Including Government Financial Institutions, State Universities and Colleges and Local Government Units) directing all heads of government offices including LGUs to organize an Internal Audit Service (IAS) in their respective offices;

DBM Budget Circular No. 2004-4, (Guidelines on the Organization and Staffing of Internal Audit Units (IAUs)); and CSC Memorandum Circular No. 12 s.2006 (Qualification standards for IAS positions) were likewise issued in connection with the establishment of an Internal Audit Unit/Service;

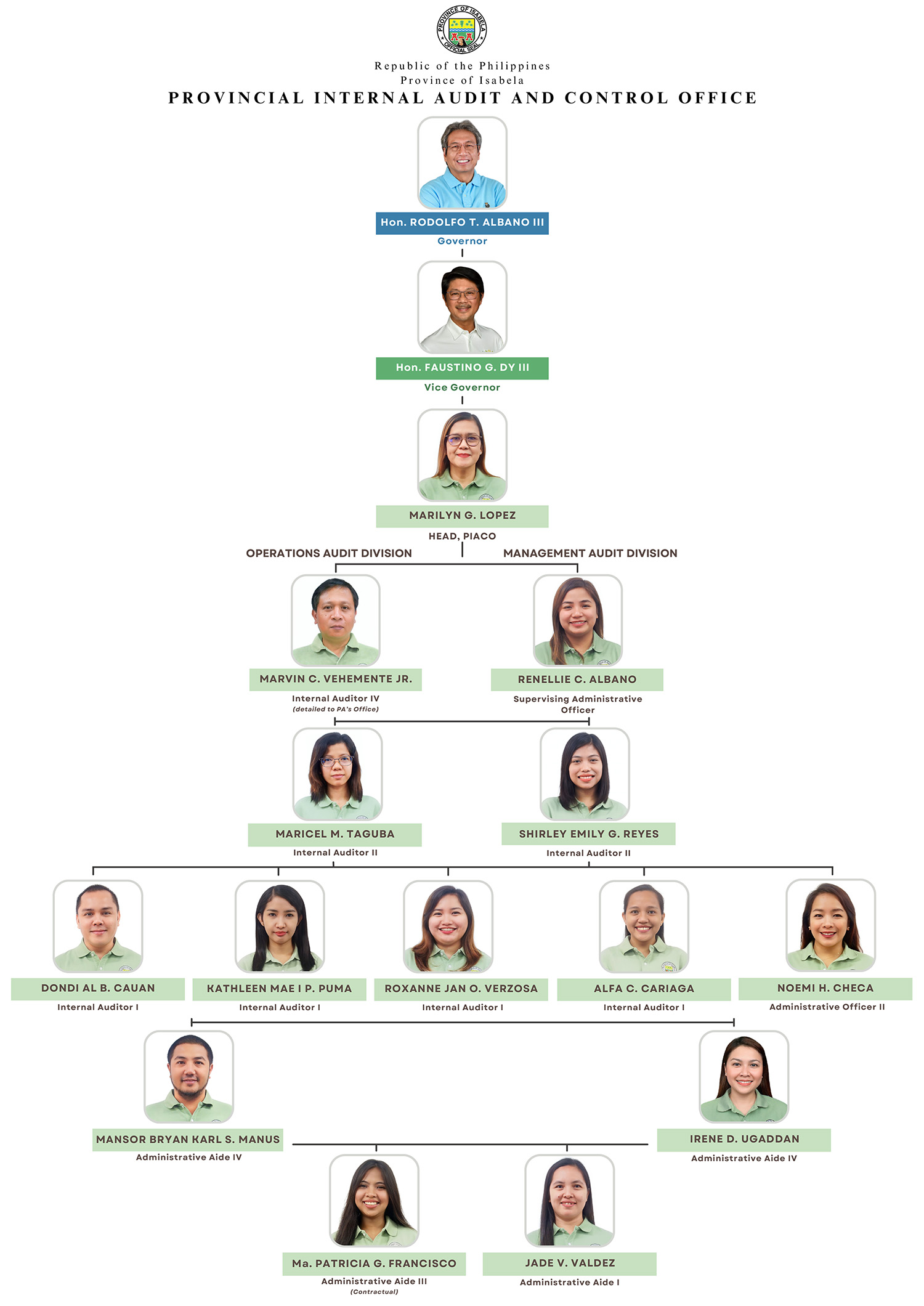

In accordance with the foregoing legal anchors and dictates, the Provincial Government of Isabela established the Provincial Internal Audit and Control Unit (PIACU) by virtue of Executive Order No. 17A Series of 2017 dated March 1, 2017. Subsequently, Appropriation Ordinance No.17 Series of 2017 dated December 19, 2017, an Ordinance authorizing the Annual Budget of the Provincial Government of Isabela was enacted creating among others the Provincial Internal Audit and Control Office (PIACO).

MANDATE:

The PIACO is mandated to conduct an evaluation or appraisal of the internal control system to determine if internal controls are well designed and properly implemented. It is also mandated to conduct compliance audit, management audit and operations audit.

VISION:

An independent, accountable and efficient Internal Audit Office committed to advancing an Efficient Government Service Delivery through an effective management controls, governance processes and operations performance.

MISSION:

To support the Provincial Government of Isabela in the effective performance of its responsibilities by appraising the effectiveness of its internal controls, thereby enhancing management controls, governance process and operations performance, in order to achieve optimum productivity and Efficient Government Service Delivery.

CORE VALUES:

Professional Competence

The PIACO maintains and applies the required professional knowledge, skills, and experience in the performance of its internal audit functions.

Integrity

The PIACO exhibits honesty, straightforwardness, and truthfulness in all of its professional and business dealings.

Accountability

The PIACO takes responsibility for all its actions, inputs and decisions.

Confidentiality

The PIACO refrains from disclosing information acquired without appropriate authorization unless there is a legal or professional obligation to do so.

Objectivity

The PIACO performs its duties without bias, conflict of interest or undue influence or its own interest.

FUNCTIONAL STATEMENT

Internal audit, as defined, is the evaluation of management controls and operations performance, and the determination of the degree of compliance with laws, regulations, managerial policies, accountability measures, ethical standards, and contractual obligations. It involves the appraisal of the plan of organization and all the coordinated methods and measures, in order to recommend courses of action on matters relating to operations and management control. Internal audit, being a separate component of internal control, is instituted to determine whether internal controls are well designed and properly operated.

The Functions of the PIACO mainly is the conduct of Management and Operations Audit to determine the degree of compliance with laws, regulations, managerial policies, accountability measures, ethical standards, and contractual obligations.

Management Audit is the separate evaluation of the effectiveness of internal controls adopted in the operating and support services units/systems to determine whether they achieve the control objectives over a period of time or as of a specific date. This includes the determination of the degree of compliance with laws, regulations, managerial policies, accountability measures, ethical standards and contractual obligations covering specific timeframes. It is a review and appraisal of the systems and processes, organizational and staffing structures, operations and management practices, records, reports, and performance standards.

Operations Audit is a separate evaluation of the outcome, output, process, and input to determine whether government operations, programs, and projects are effective, efficient, ethical and economical including compliance with laws regulations, managerial policies, accountability measures, ethical standards and contractual obligations. It involves an evaluation of whether or not performance targets and expected results were achieved.

Accomplishment Reports

ANNUAL

- 2024 Annual Accomplishment Report

- 2023 Annual Accomplishment Report

- 2022 Annual Accomplishment Report

- 2021 Annual Accomplishment Report

- 2020 Annual Accomplishment Report

- 2019 Annual Accomplishment Report

- 2018 Annual Accomplishment Report

MONTHLY

2025

- PIACO Accomplishment Report for March 2025

- PIACO Accomplishment Report for February 2025

- PIACO Accomplishment Report for January 2025

2024

- PIACO Accomplishment Report for December 2024

- PIACO Accomplishment Report for November 2024

- PIACO Accomplishment Report for October 2024

- PIACO Accomplishment Report for September 2024

- PIACO Accomplishment Report for August 2024

- PIACO Accomplishment Report for July 2024

- PIACO Accomplishment Report for June 2024

- PIACO Accomplishment Report for May 2024

- PIACO Accomplishment Report for April 2024

- PIACO Accomplishment Report for March 2024

- PIACO Accomplishment Report for February 2024

- PIACO Accomplishment Report for January 2024

2023

- PIACO Accomplishment Report for December 2023

- PIACO Accomplishment Report for November 2023

- PIACO Accomplishment Report for October 2023

- PIACO Accomplishment Report for September 2023

- PIACO Accomplishment Report for August 2023

- PIACO Accomplishment Report for July 2023

- PIACO Accomplishment Report for June 2023

- PIACO Accomplishment Report for May 2023

- PIACO Accomplishment Report for April 2023

- PIACO Accomplishment Report for March 2023

- PIACO Accomplishment Report for February 2023

- PIACO Accomplishment Report for January 2023

2022

- PIACO Accomplishment Report for December 2022

- PIACO Accomplishment Report for November 2022

- PIACO Accomplishment Report for October 2022

- PIACO Accomplishment Report for September 2022

- PIACO Accomplishment Report for August 2022

- PIACO Accomplishment Report for July 2022

- PIACO Accomplishment Report for June 2022

- PIACO Accomplishment Report for May 2022

- PIACO Accomplishment Report for April 2022

- PIACO Accomplishment Report for March 2022

- PIACO Accomplishment Report for February 2022

- PIACO Accomplishment Report for January 2022

2021

- PIACO Accomplishment Report for December 2021

- PIACO Accomplishment Report for November 2021

- PIACO Accomplishment Report for October 2021

- PIACO Accomplishment Report for September 2021

- PIACO Accomplishment Report for August 2021

- PIACO Accomplishment Report for July 2021

- PIACO Accomplishment Report for June 2021

- PIACO Accomplishment Report for May 2021

- PIACO Accomplishment Report for April 2021

- PIACO Accomplishment Report for March 2021

- PIACO Accomplishment Report for February 2021

- PIACO Accomplishment Report for January 2021

2020

- PIACO Accomplishment Report for December 2020

- PIACO Accomplishment Report for November 2020

- PIACO Accomplishment Report for October 2020

- PIACO Accomplishment Report for September 2020

- PIACO Accomplishment Report for August 2020

- PIACO Accomplishment Report for July 2020

- PIACO Accomplishment Report for June 2020

- PIACO Accomplishment Report for May 2020

- PIACO Accomplishment Report for April 2020

- PIACO Accomplishment Report for March 2020

ISO 9001:2015 Surveillance Audit

February 5, 2024

ISO 9001 : 2015 Certification

ISO 9001 : 2015 Internal Quality Audit and Training

July 18, 2018

https://provinceofisabela.ph/index.php?option=com_content&view=article&layout=edit&id=417#sigFreeId3ac9087e1a

ISO 9001 : 2015 Awareness and Risk Management Training

April 24-25, 2018

https://provinceofisabela.ph/index.php?option=com_content&view=article&layout=edit&id=417#sigFreeIdb2de5c957d